on the main news in the world of wine and wineries, with a strategic eye for those working in the sector.

Recent Key Points

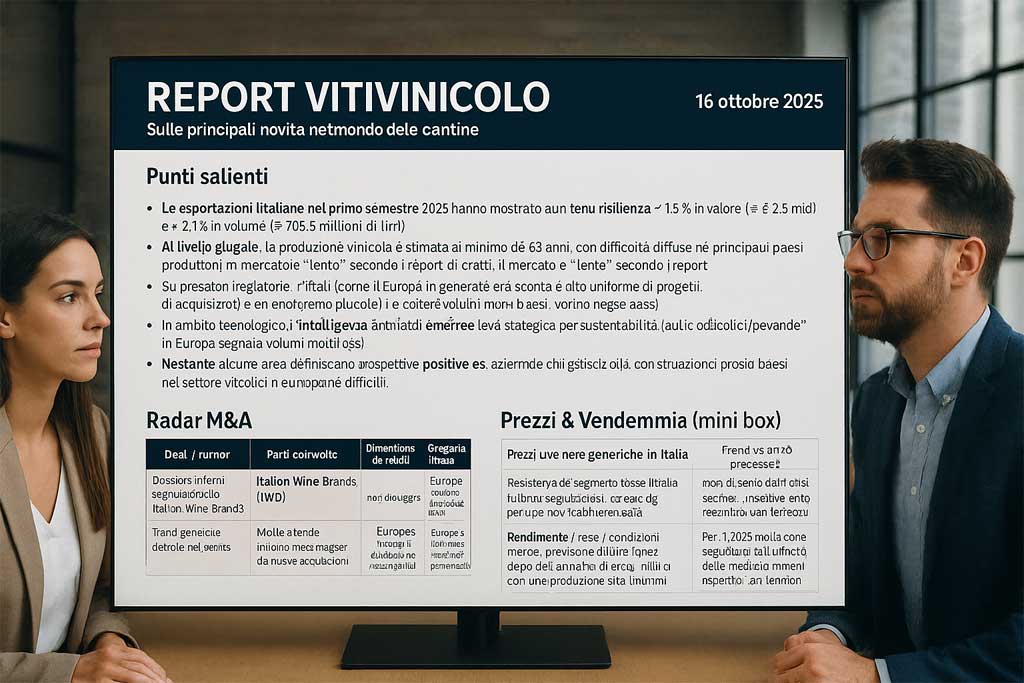

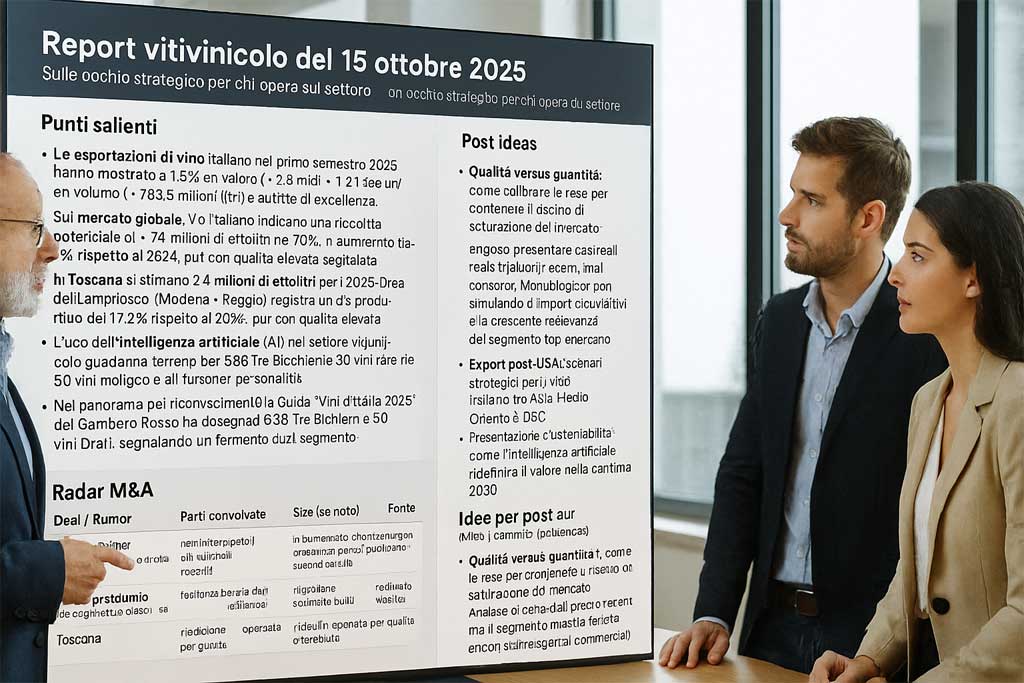

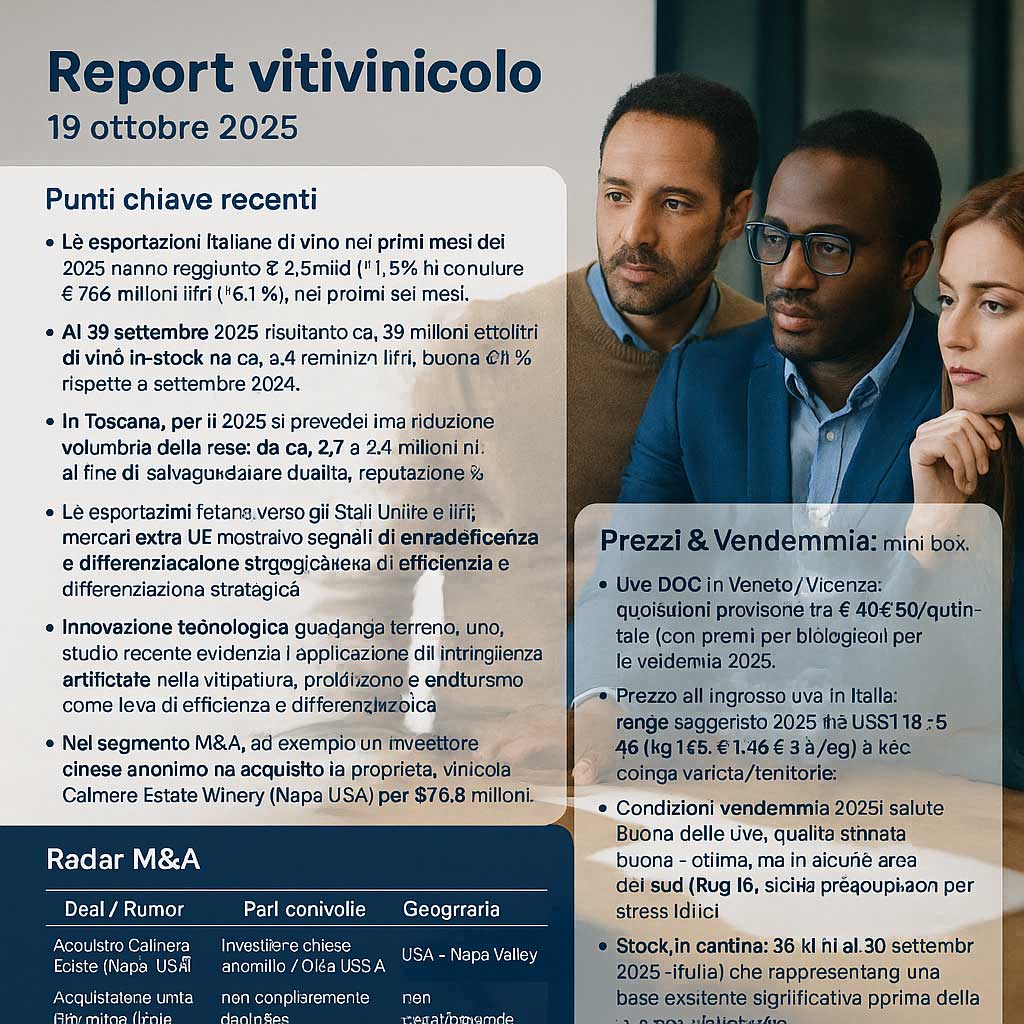

- Italian wine exports in the first months of 2025 reached approximately €2.8 billion (1.5% in value) and 703 million litres (2.1%) in the first six months.

- As of September 30, 2025, there were approximately 36 million hectoliters of wine in stock in Italian wineries: a 9.6% decrease compared to July but a 1.3% decrease compared to September 2024.

- The 2025 Italian harvest is estimated at 47.4 million hectolitres (8% compared to 2024), with generally good-excellent quality but with signs of overproduction and pressure on prices.

- In Tuscany, a voluntary reduction in yields is expected for 2025, from approximately 2.7 to 2.4 million hl, in order to safeguard quality, reputation and average price.

- Italian exports to the United States and other non-EU markets are showing signs of weakness: in July 2025, a decline of -0.9% in value and -3.4% in volume compared to 2024.

- Technological innovation is gaining ground: a recent study highlights the application of artificial intelligence in viticulture, production, and wine tourism as a lever for efficiency and strategic differentiation.

- In the M&A segment, for example, an anonymous Chinese investor acquired the Calmére Estate Winery (Napa USA) for $16.8 million in cash , with plans to expand into Asia.

M&A Radar

| Deal / Rumor | Parties involved | Size (if known) | Geography | Source & date |

|---|---|---|---|---|

| Purchase Calmére Estate (Napa, USA) | Anonymous Chinese investor / Peju family | approximately US$ 16.8 M | USA – Napa Valley | |

| Acquisition of the Valle Talloria production unit by Caffo Group 1915 | Caffo Group acquires Italian Wine Brands’ Piedmont operations | not fully detailed | Italy – |

Prices & Harvest: mini-box

- DOC grapes in Veneto/Vicenza: provisional prices between €40-€60/quintal (with premiums for organic) for the 2025 harvest.

- Wholesale grape prices in Italy: suggested range 2025 between US$1.19-5.46/kg (approx. €1.10-€5/kg) depending on variety/territory.

- 2025 harvest conditions: good grape health, estimated good-excellent quality, but in some areas of the South (Puglia, Sicily) concerns about water stress.

- Cellar stock: 36 Mhl as of September 30, 2025 (Italy) representing a significant existing base before the new harvest.

- Trend: with the harvest increasing (8%) and stocks already high, strong pressure is expected on the prices of both grapes and bulk wine if not accompanied by action to contain yields or diversify markets.