(Focus on Italy, global coordination for winery/consortium decisions and M&A).

Key updates

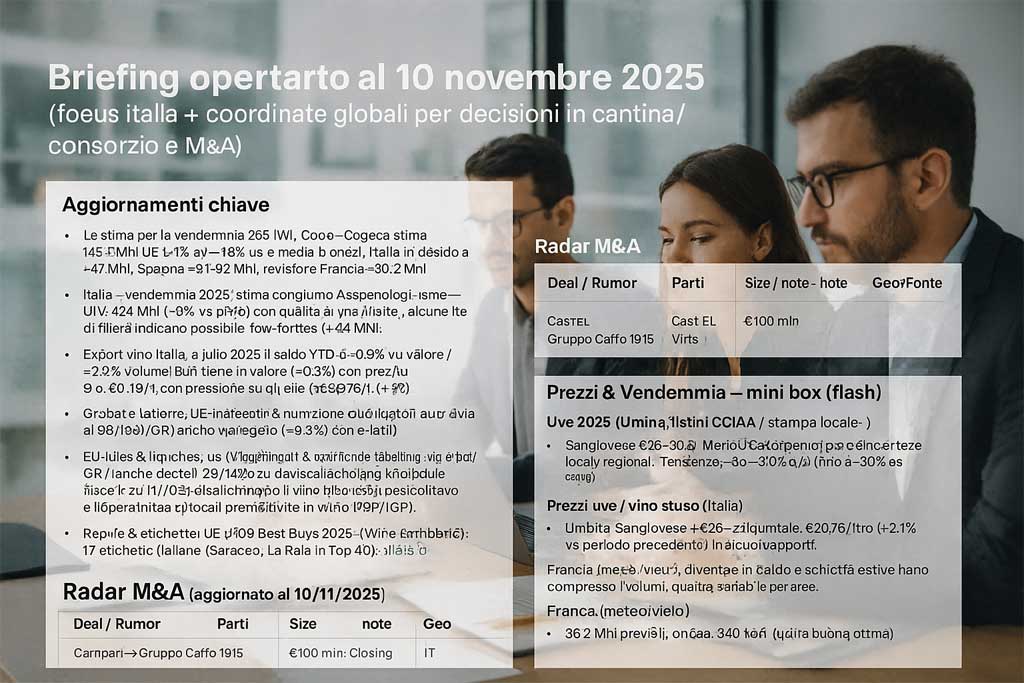

– In Europe, Copa Cogeca raises its production estimate for EU wine in 2025 to 145.5 Mhl (1% vs 2024), but still approximately ‑7.5% below the five-year average.

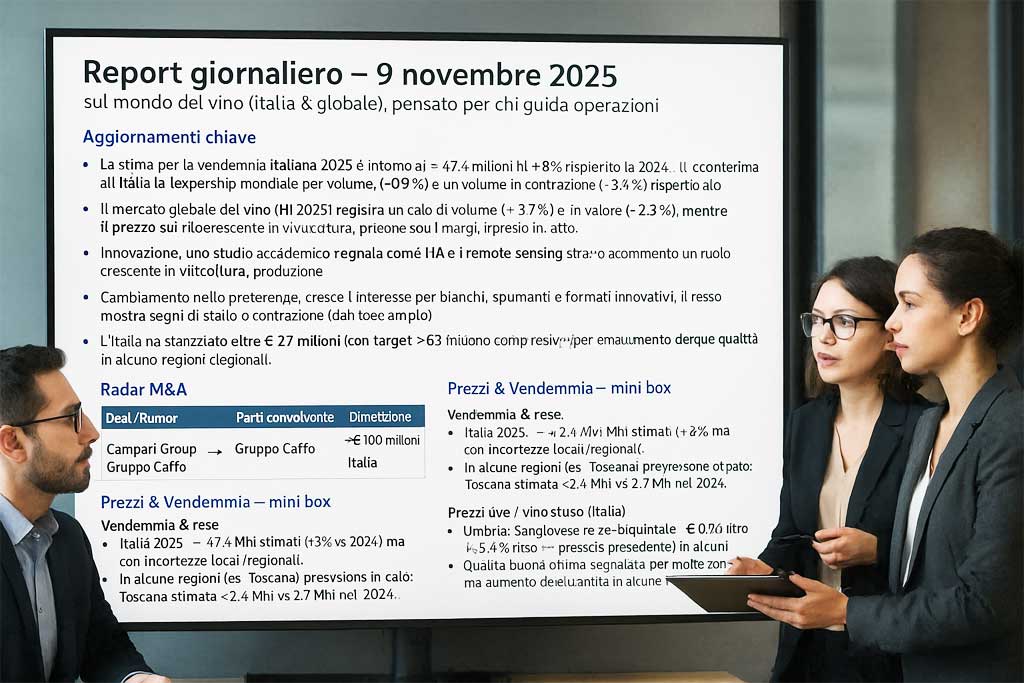

– In Italy, the joint estimate by Assoenologi / ISMEA / Unione Italiana Vini points to ~ 47.4 Mhl (8% vs 2024) with quality judged good-excellent; however, some industry sources report an “adjustment towards low forties”.

– Italian exports (Jan-Jul 2025): value -0.9% / volume -3.4%. In the USA, due to 15% tariffs, a decrease in value of approximately -28% in the two-month period July-Aug.

– Italian stocks as of 09/30/2025: approximately 36 Mhl , -9.6% compared to July but 1.3% on an annual basis → signals residual stock and potential pressure on bulk wine and generic grape margins.

– In global wine trade H1 2025: value 2.3%, volume 3.7%. The “bulk wine” segment held up better: 0.3% in value and estimated average price ~€0.78/L (2.1%).

– On the regulatory front: the EU will require mandatory ingredients and nutritional information for wine starting in December 2023, with the option of e-labeling/QR; the OIV has updated its 2025 standards on practices and labeling; in Italy, decrees of 20/12/2024 and 14/05/2025 regulate the production of (partially) dealcoholized wine and its use in mixed-use premises.

– Speaking of awards, Wine Enthusiast’s “Top 100 Best Buys 2025” ranking includes 17 Italian labels , with brands like Saracco and La Raia in the Top 10, strengthening Italy’s quality/price positioning in the premium segment.

M&A Radar

| Deal / Rumor | Parts | Size | Geo | Source |

|---|---|---|---|---|

| Transfer of the Cinzano & Frattina brands | Campari Group → Caffo Group 1915 | ~€100 million | Italy | Reuters June 26, 2025 |

| Tannico Acquisition | CASTEL Vins ↔︎ Tannic | ND | Italy/France | Forvis/Mazars press release, October 6, 2025 |

| Binding offer for Valle Talloria (former Giordano complex) | Caffo Group 1915 ↔︎ Italian Wine Brands | ND | Italy (Piedmont) | IWB press release 09 Oct 2020 |

Prices & Harvest

- Italian Grapes (examples, October price lists): Sangiovese ~ €26-30/q ; Merlot/Cabernet ~€28-30/q; Sagrantino DOCG ~€100-140/q. Trend: ~30% y/y; in some cases up to 50% vs. 2023; with the exception of Trebbiano Spoletino, which is rising sharply due to scarcity.

- Global bulk wine H1 2025: average price ≈ €0.78/L (2.1% vs previous year) in a context of weak trade and cautious demand.

- Italian stocks as of September 30, 2025: ~36 Mhl; estimated harvest ~47.4 Mhl (quality declared good/excellent) but risk of reductions in some areas due to weather/yield; in France, the harvest forecast is ~36.2 Mhl, influenced by heat waves and summer drought.

- Implications: pressure on bulk and generic grape margins, opportunities for premium segments and labeling/packaging innovation.