Daily wine & cellar briefing.

Key points

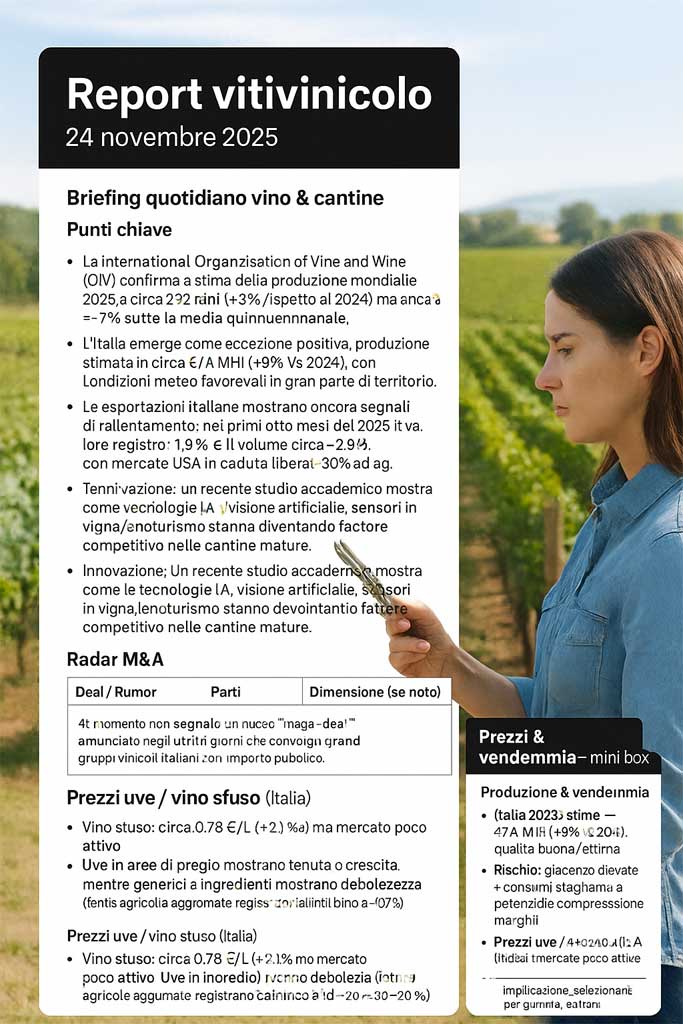

- The International Organisation of Vine and Wine (OIV) confirms its estimate of world production in 2025 at around 232 Mhl (3% compared to 2024) but still ≈-7% below the five-year average , due to repeated climate shocks.

- Italy emerges as a positive exception: production estimated at around 47.4 Mhl (8% vs 2024), with favorable weather conditions across much of the country.

- Italian exports are still showing signs of slowing: in the first eight months of 2025, value recorded -1.9% and volume around -2.9% , with the US market in free fall (-30% in August).

- The global export wine market is contracting: volumes are falling (-3.7% in 1H 2025 vs 1H 2024) and values are slightly down (-2.3%), a sign of an “era of less but better”.

- Prices and inventories: In Italy, increased production combined with high inventories heralds the risk of margin pressure; the average bulk wine price remains around €0.78/L (2.1% year-on-year), but the market remains relatively inactive.

- Innovation: A recent academic study shows how AI, computer vision, and sensor technologies in the vineyard/wine tourism sector are becoming a competitive factor in mature wineries.

- M&A strategy & positioning: The Italian market is seeing more selective deals (premium, tech, export) and less focus on pure volume. Wineries must focus on quality, brand, and channels rather than quantity. (Multiple sources)

M&A Radar

| Deal / Rumor | Parts | Size (if known) | Geography | Strategic note |

|---|---|---|---|---|

| — | — | — | — | I’m not currently reporting any new “megadeal” announced in recent days involving major Italian wine groups with public funding. However, the trend is clear: acquisitions geared toward premium brands, digital platforms, and exports. |

Prices & Harvest – mini box

Production & Harvest

- Italy 2025: estimate ~47.4 Mhl (8% vs 2024); good/excellent quality.

- Risk: High inventories, stagnant consumption = potential margin compression.

Grape / bulk wine prices (Italy)

- Bulk wine: approximately €0.78/L (2.1% y/y) but the market is not very active.

- Grapes in premium areas are showing signs of holding up or growing, while generics and ingredients are showing weakness (updated agricultural sources record drops of up to -10/-20%).

- Implication: select by range, avoid indiscriminate production in overcapacity conditions.